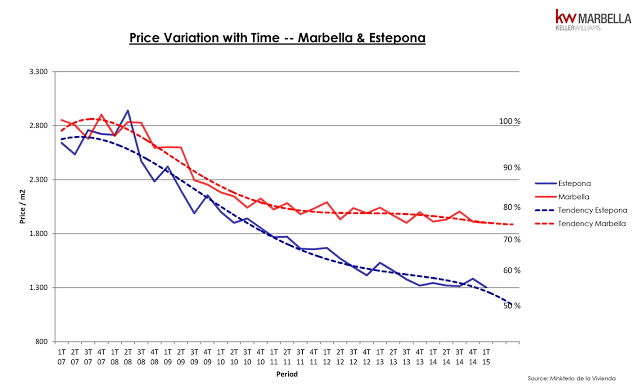

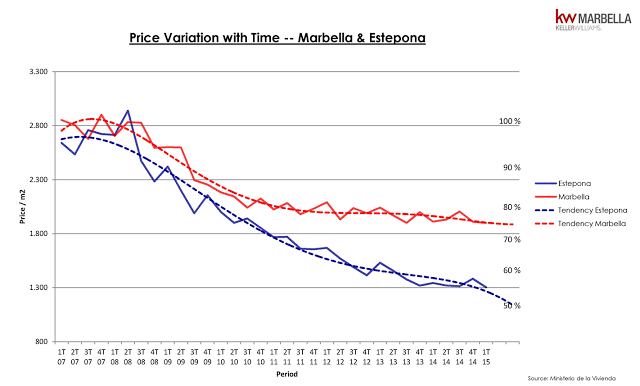

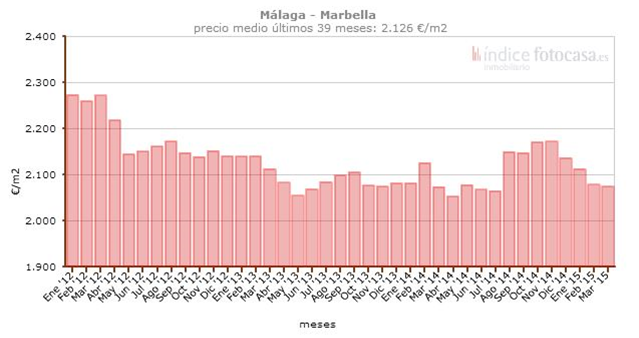

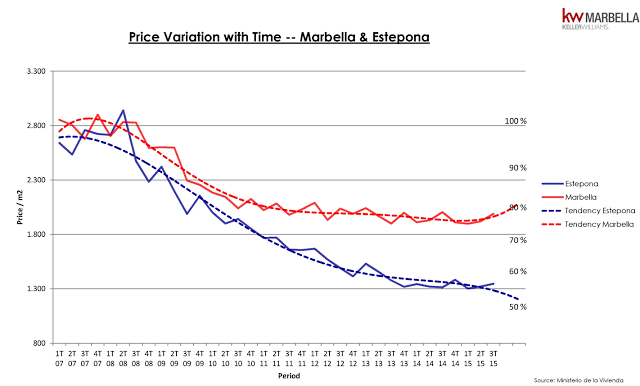

In the last month of December, the price index for the third quarter of year 2015 was published by the Ministry of Housing showing, in Marbella, two consecutive quarters of increases. The increases are not great but at least it is a change in the tendency as shown in the tendency line of the prices. However, the prices are still a little bit lower than one year before.

We saw the same scenario in 2014 and the tendency never materialized but this could be the year of the inflexion point. A number of analyst have already predicted that 2016 is going to be the year of the consolidation, stabilization and normalization of the real estate market in Spain with potential increases between 4 and 6% with some analysts going as high as 10% increases. The improvement on the unemployment numbers, the reduction on the mortgage rates, the continuous recovery of the economy in general, that we hope will not be affected by the political instability, and the reduced prices are the catalysts of the increase of the demand, specially the Spanish one, highly reduced in the last years, and, as a consequence, of the prices.

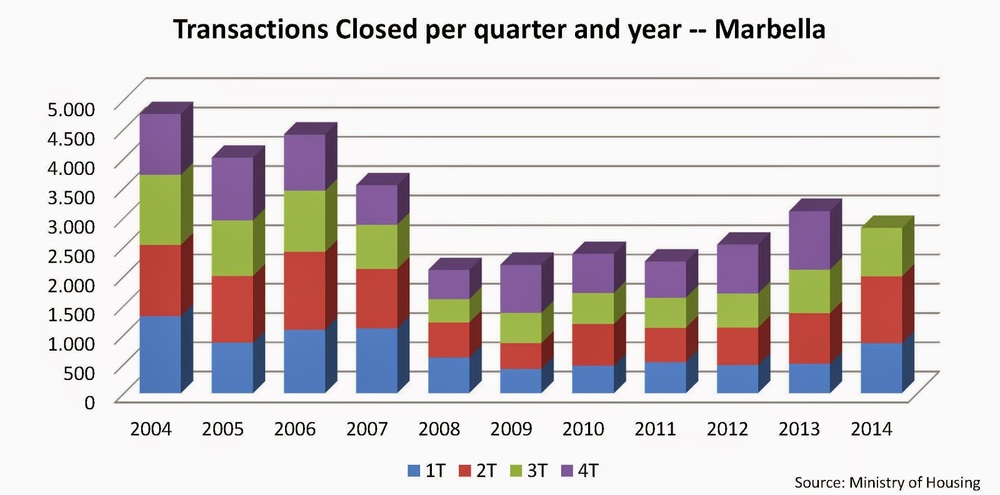

If we take a look to the chart besides, CaixaBank is already predicting a return to the positive market of 2005 and 2006, i.e. increase in sales and increase in prices.

Finally, a little comment on Estepona where the prices are still going down. Marbella has a better name than Estepona and the higher demand helped to stop the fall in prices. We should also see in Estepona the stabilization in prices commented above.