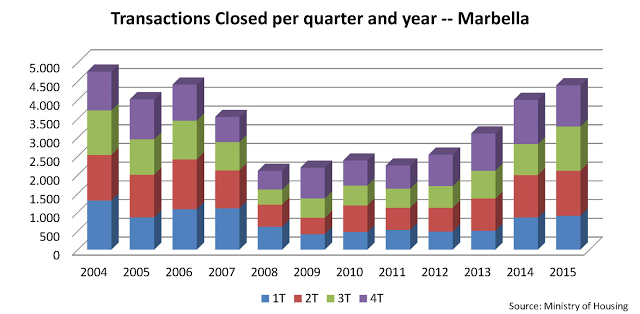

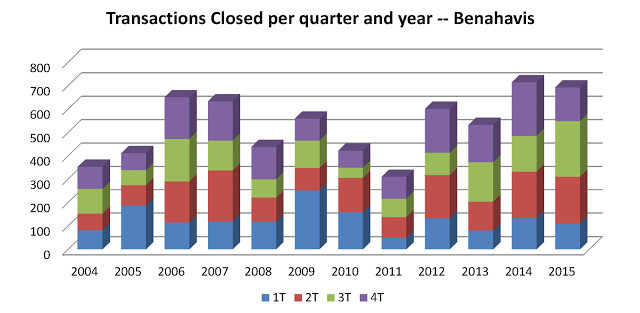

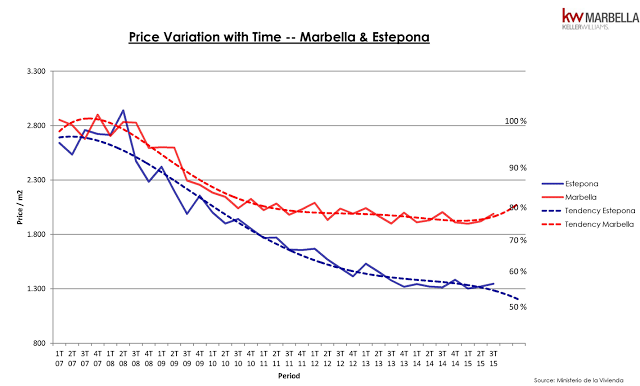

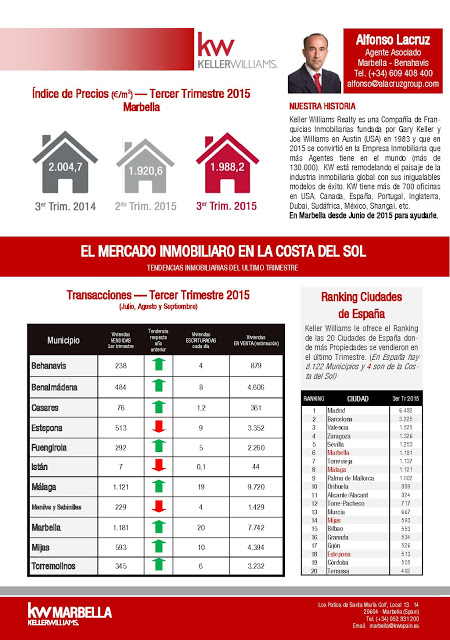

El Ministerio de Fomento acaba de publicar el índice de precios para el primer trimestre de 2016 con buenas noticias para todos nosotros salvo, quizás, para los compradores, ya que el aumento en los precios para Marbella y Estepona parece estar, poco a poco, consolidándose. Con base interanual y por primera vez desde 2008, se ven aumentos en el índice de precios de un 4% para Marbella y Estepona.

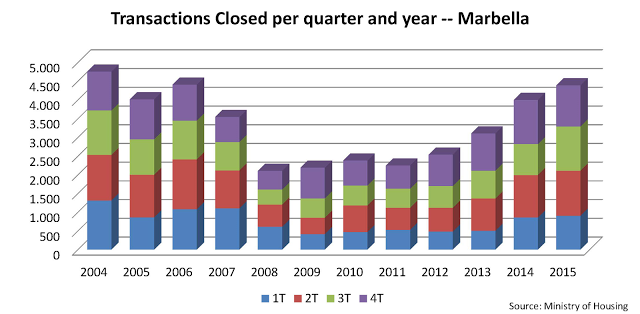

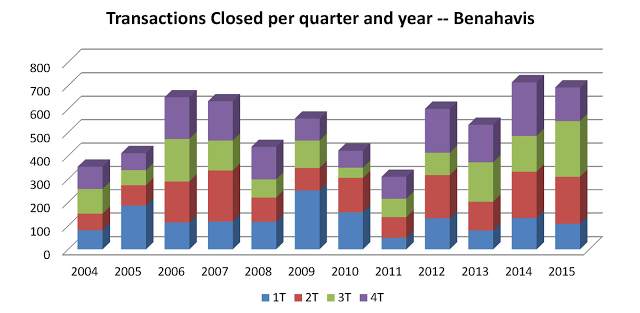

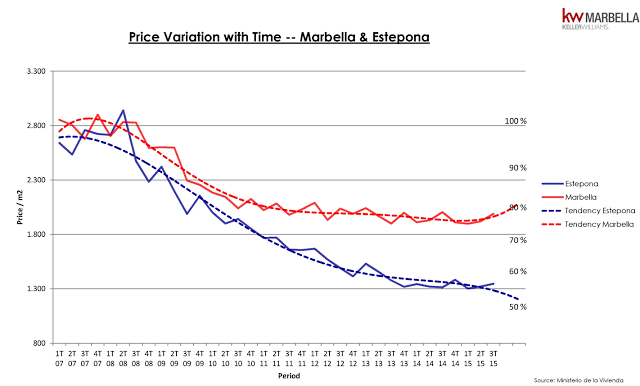

He comentado en numerosas ocasiones sobre esta cuestión, y la última, el pasado enero, cuando todavía el crecimiento no estaba claro sobretodo viendo las sensaciones en la calle. Aunque el mercado sigue aún lento, parece que la tendencia al alza de los precios ya está aquí. Si se observa, el gráfico adjunto, se ve que en todas las localidades alrededor de Marbella, excepto por Fuengirola, los precios parecen haber empezado a subir. Para verlo aún mejor, he recopilado en el gráfico que se encuentra debajo, año por año, el incremento del índice de precio en las mismas localidades en los últimos tres años y podemos ver claramente la diferencia: en 2013 hubo un descenso medio aproximado del 10%, un mínimo descenso en 2014 como año de transición y aumentos en 2015. Todavía es un aumento moderado de un 4% pero lo importante es el cambio en la tendencia. Algunos analistas ya predijeron el mismo aumento para 2016 y parece ser cierto. Espero que la inestabilidad política en España y las elecciones no afectarán este renacer.