What the latest data means for sellers, buyers and investors?

Sales fell. Prices rose. In Q4 2025, the Costa del Sol delivered a contradiction that tells a different story to each of the three readers who matter most: the seller thinking of listing, the buyer still hesitating, and the investor de-ciding where to allocate next.

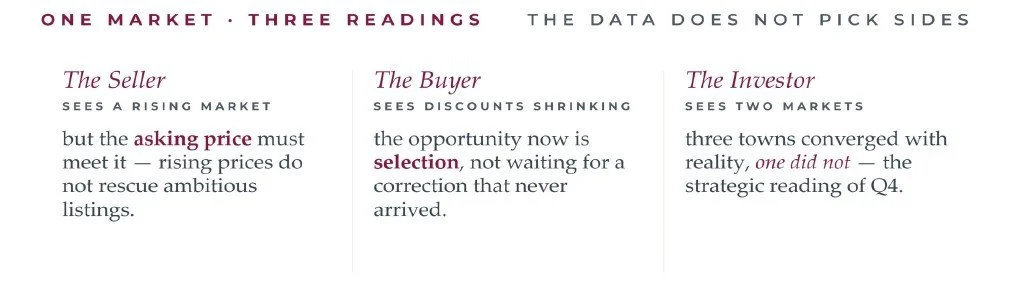

For the Seller. The official figures are encouraging: sold prices climbed across all four municipalities, and the gap between asking and sold prices is narrowing in Marbella, Benahavís and Estepona. That only happens when realistic sellers meet the market and ambitious ones do not. A property that has been listed for many months without movement is not being failed by the market, it is being failed by its asking price.

For the Buyer. The room for meaningful negotiation is shrinking. In Marbella, sold prices rose 3.2% in Q4 alone while asking prices rose only 2.1% so the real market is moving faster than seller expectations. On properties priced sensibly from day one, the ones that actually transact, discounts have become minimal. The correc-tion some buyers were waiting for has not arrived, and the window for waiting productively is narrowing with each quarter. The opportunity now lies in selection: identifying the right property in the right micro-location at a fair price, rather than holding out for a discount the data no longer supports.

For the Investor. The most useful signal this quarter is the divergence between Mijas and the other three mu-nicipalities. In Marbella, Benahavís and Estepona, the gaps between asking and sold prices stand at 31.4%, 42.5% and 23.9% respectively, all trending downward. These are markets where reality has been absorbed, and disciplined entry is rewarded over speculative timing.

Mijas is the exception: the gap is only 8.5%, but it is widening rather than closing, with asking prices rising fast-er than sold prices. That is not an opportunity, it is a market where sellers have not yet adjusted. The disciplined approach is to watch it closely and enter only with precision, zone by zone, rather than on aggregate numbers.

One market. Three readings. The data does not pick sides, the reader does.