While long-term value remains exceptionally strong on the Costa del Sol. the market has reached a stage where seller expectations are drifting from buyer reality. Our latest data confirms that serious, informed buyers are still active but increasingly selective. This shift has widened the "Negotiation Gap," the space between the advertised asking price and the final closing price, now the key factor affecting liquidity and sales speed in the luxury segment.

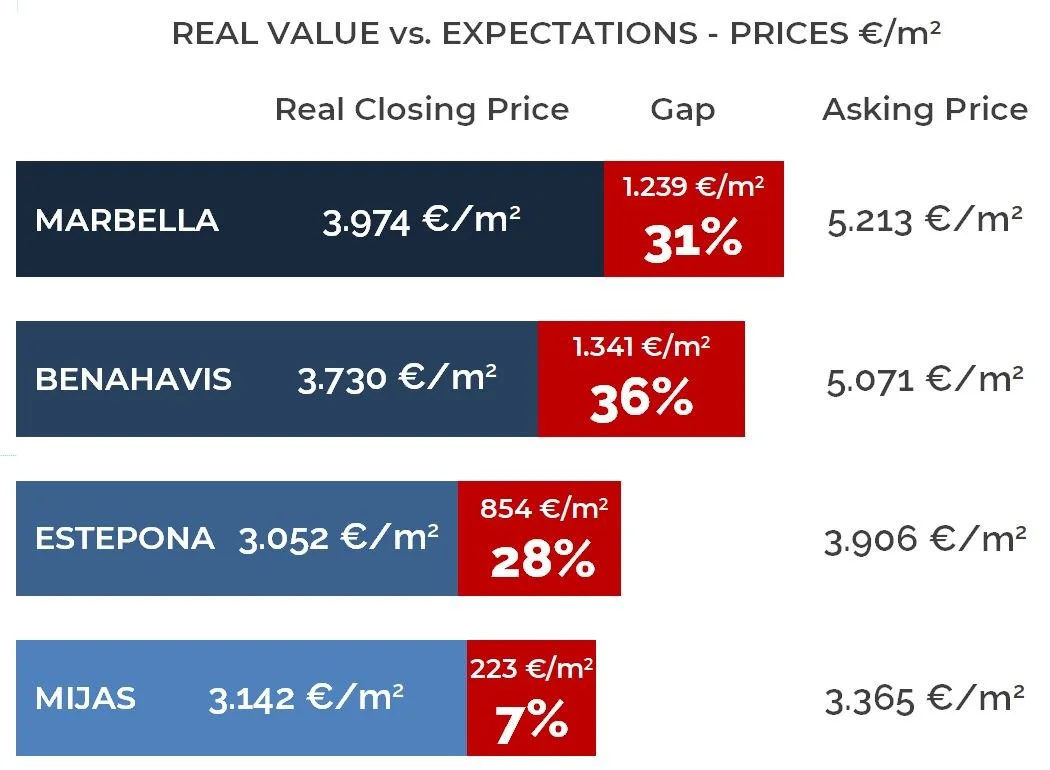

1. The Excessive Gap: Expectations vs Market Value. The divergence between the Asking Price and the Closed Price (Land Registry) is the main reason transactions are slowing. The figures are striking: in Benahavis, the negotiation gap stands at 36%, equivalent to €1,341 per square meter, Marbella follows at 31% (€1,239/m2) and Estepona at 28%. These differences clearly show that many homes enter the market with asking prices buyers simply reject.

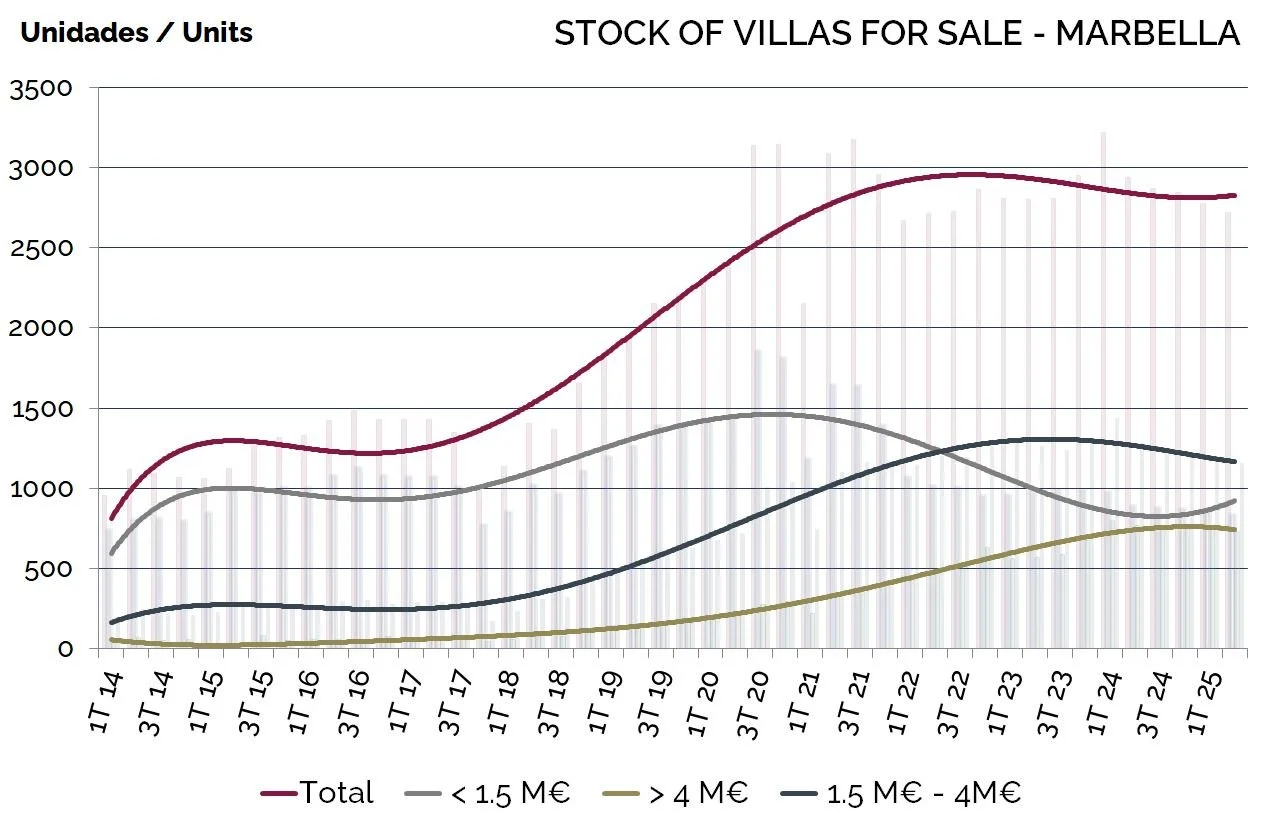

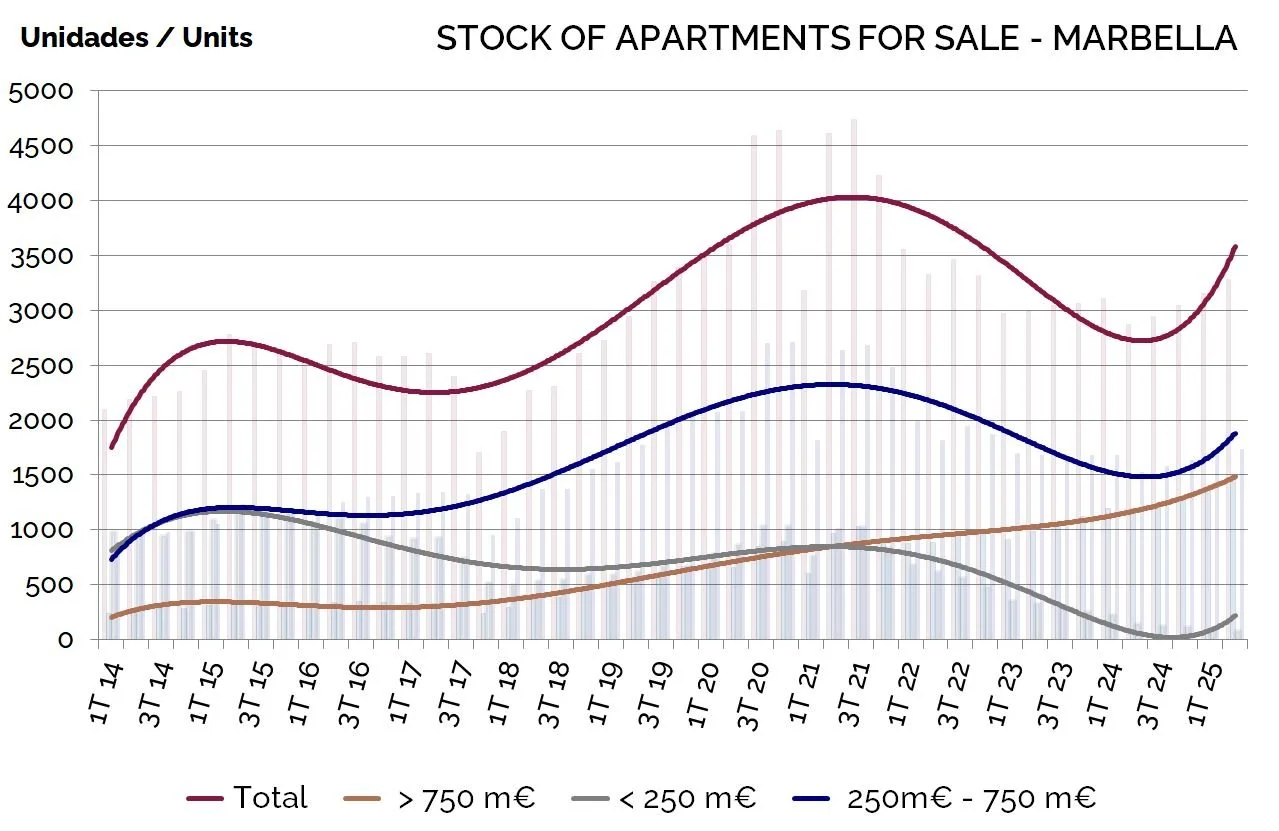

2. Market Friction and a Slower Sales Pace. This widening gap has led to a noticeable slowdown. Closed transactions in Marbella, Benahavís, and Mijas dropped by around 20% in Q2 2025 compared with the previous year. Marbella alone saw a 20.9% decline in units sold versus Q2 2024. Overpriced listings remain longer on the market. eroding buyer confidence and reducing overall momentum. The result is a cycle of inefficiency that slows the entire market.

3. The Solution: Price Coherence Protects Value. To reverse this trend, sellers must embrace realistic pricing from the start. Overpricing weakens negotiating power and often leads to harder final discounts. By contrast. properties priced in line with real demand attract serious buyers quickly and close closer to their asking value. A coherent valuation is not just a recommendation - it's a vital strategy to ensure a swift, secure sale and protect your capital.

In summary, demand remains robust and long-term fundamentals are strong, but achieving success today requires strategic, marketcoherent pricing that bridges the growing negotiation gap.