Journal on the Real Estate Market on the Costa del Sol - June 2026

WHAT TAXES DO YOU PAY WHEN SELLING A PROPERTY IN MARBELLA & BENAHAVÍS? (2026)

There are two main taxes when you sell in Spain: the Capital Gain Tax, paid to the national tax office on your profit, and the Plusvalia, paid to your Town Hall on the increase in the value of the land. These are the general rules for individuals; particular cases vary.

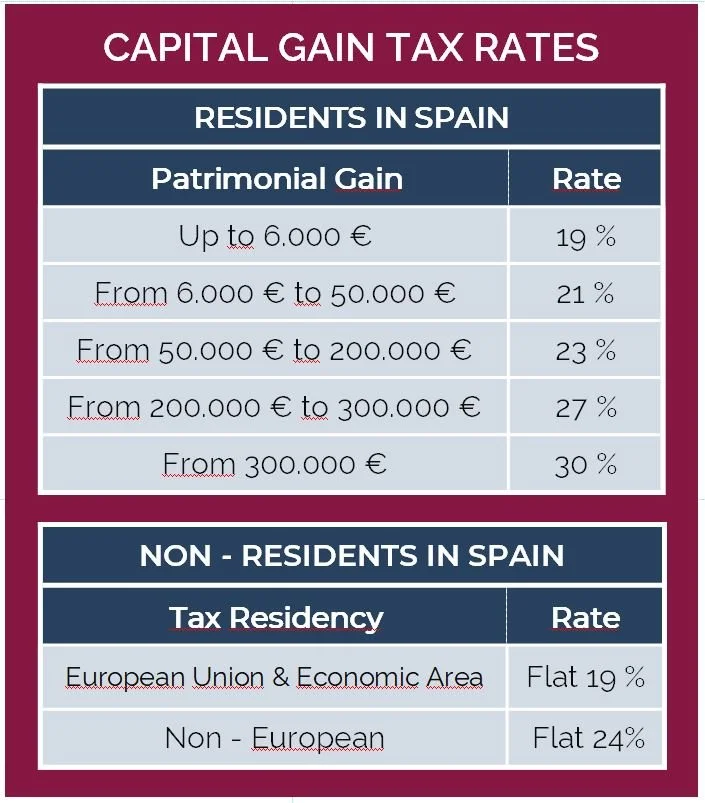

CAPITAL GAIN TAX

1. How is the taxable gain calculated?

Patrimonial Gain = Value Transferred - Acquisition Value

Value Transferred is the price you sell for, minus the costs of the sale: agency fees with their VAT, the Plusvalia, and the cancellation of the mortgage if there was one.

Acquisition Value is the price you originally paid, plus the costs of that purchase: notary and land registry fees, and the Transfer Tax, or the VAT and Stamp Duty if it was a new build. You may also add any extension or substantial improvement, provided you hold the invoices. Ordinary repairs do not count, and without an invoice nothing counts.

2. When is it paid?

Residents, within their income tax return (IRPF), in June of the year following the sale. Non-residents, within four months of closing.

3. What are the rates in 2026?

For residents it is progressive and flat for non-residents (see attached table). The buyer must also withhold 3% of the price at the Notary as an advance on that tax. If the final bill is lower, the difference is refunded, normally within six to twelve months.

PLUSVALIA TAX

4. Who pays it, and when?

The seller, unless agreed otherwise, within 30 working days of the deed. There are two ways to calculate it and you may use whichever gives the lower result.

Direct estimation. Based on your real gain, applying the proportion the land represents within the cadastral value. Sell for less than you paid and the tax is zero, although you must still declare it.

Objective system. Cadastral value of the land x coefficient x municipal rate. The coefficient depends on the years of ownership; the rate is capped at 30%.

Worth knowing this year: the coefficients were raised in January 2026, but Parliament repealed the decree on 27 January and the previous ones apply again.

In short: what you take home depends not only on your asking price but also on the invoices you kept and the year you bought.

* As each case is different, this article is only a brief note and deductions may also apply, it is highly recommended that you check your own details with your lawyer or tax advisor.

¿QUÉ IMPUESTOS SE PAGAN AL VENDER UNA PROPIEDAD EN MARBELLA Y BENAHAVÍS? (2026)

Al vender un inmueble en España hay dos impuestos principales a liquidar: la Ganancia Patrimonial, pagable a Hacienda por el beneficio obtenido, y la Plusvalía Municipal, que se paga al Ayuntamiento por el aumento del valor del suelo. Estas son las reglas generales para particulares que podrían tener variaciones por caso.

GANANCIA PATRIMONIAL (IRPF)

1. ¿Cómo se calcula el beneficio que tributa?

Ganancia Patrimonial = Valor de Transmisión - Valor de Adquisición

El Valor de Transmisión es el precio al que vende, menos los gastos de la venta: los honorarios de la agencia con su IVA, la Plusvalía, y la cancelación de la hipoteca si la hubiera.

El Valor de Adquisición es el precio que pagó al comprar, más los gastos de aquella compra: notaría y registro, y el Impuesto de Transmisiones, o el IVA y Actos Jurídicos Documentados si era obra nueva. También puede sumar cualquier ampliación o mejora sustancial, siempre que conserve las facturas. Las reparaciones ordinarias no cuentan, y sin factura no cuenta nada.

2. ¿Cuándo se paga?

Los residentes, en la declaración de la renta (IRPF), en junio del año siguiente a la venta. Los no residentes, dentro de los cuatro meses posteriores a la firma.

3. ¿Cuáles son los tipos en 2026?

Para residentes es progresivo y fijo para no-residentes (ver tabla). Además, el comprador está obligado a retener un 3% del precio en la Notaría como anticipo de ese impuesto. Si la cuota final es menor, se devuelve la diferencia, normalmente en un plazo de seis meses a un año.

PLUSVALÍA MUNICIPAL

4. ¿Quién la paga y cuándo?

El vendedor, salvo pacto en contrario, dentro de los 30 días hábiles tras la firma. Desde 2021 hay dos formas de calcularla y puede aplicar la que le resulte más baja.

Estimación directa. Según la ganancia real, aplicando la proporción que representa el suelo dentro del valor catastral. Si vende por menos de lo que pagó, el impuesto es cero, aunque igualmente hay que declararlo.

Sistema objetivo. Valor catastral del suelo x coeficiente x tipo municipal. El coeficiente depende de los años de tenencia; el tipo tiene un máximo del 30%.

Un apunte de este año: los coeficientes se subieron en enero de 2026, pero el Congreso derogó el decreto el 27 de enero y vuelven a aplicarse los anteriores.

En resumen: lo que se lleva depende no solo de su precio de salida sino también de las facturas que guardó y del año en que compró.

* Como cada caso es diferente, el artículo es genérico y pueden aplicar deducciones, es recomendable que consulte los detalles con su abogado o asesor fiscal.

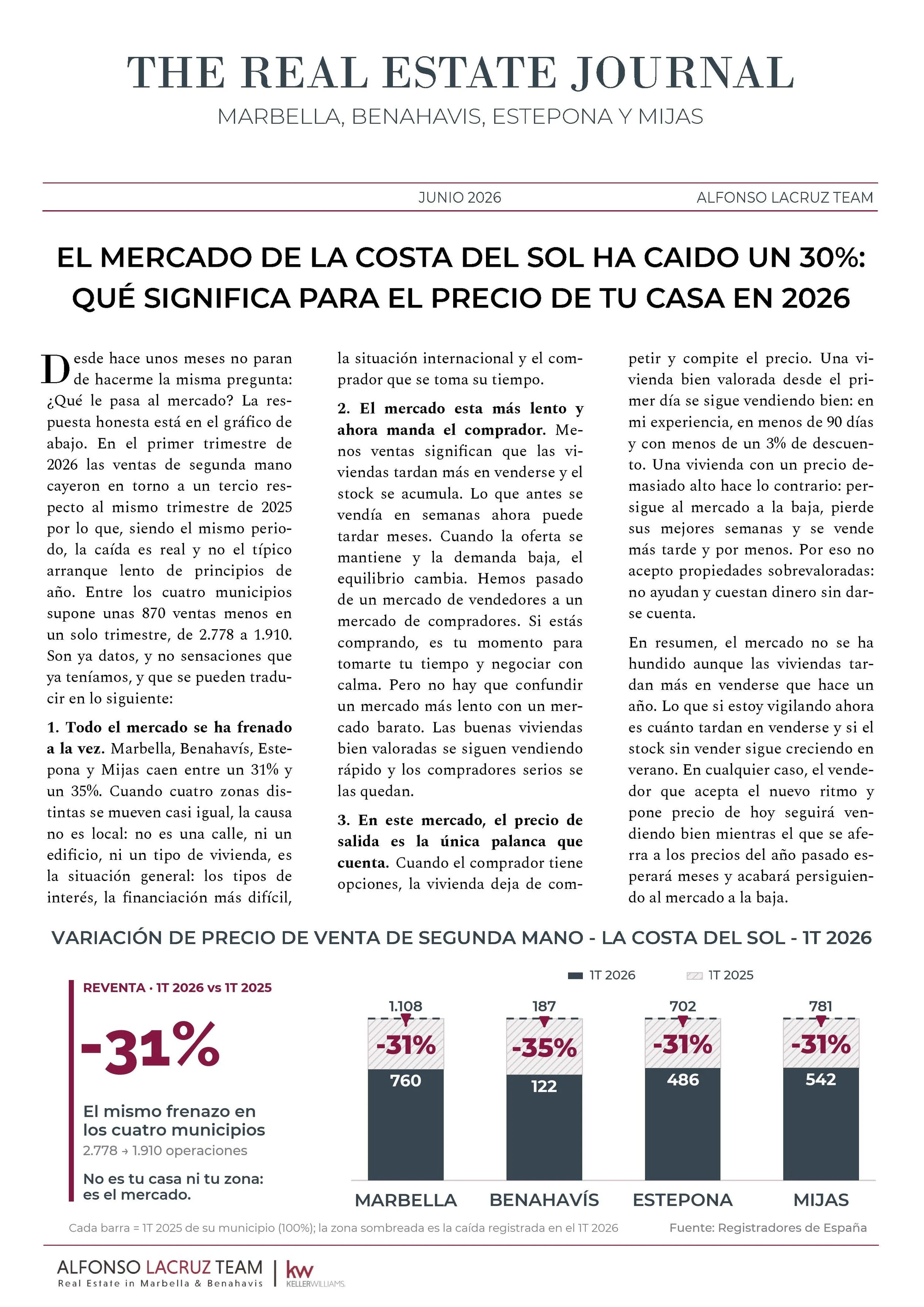

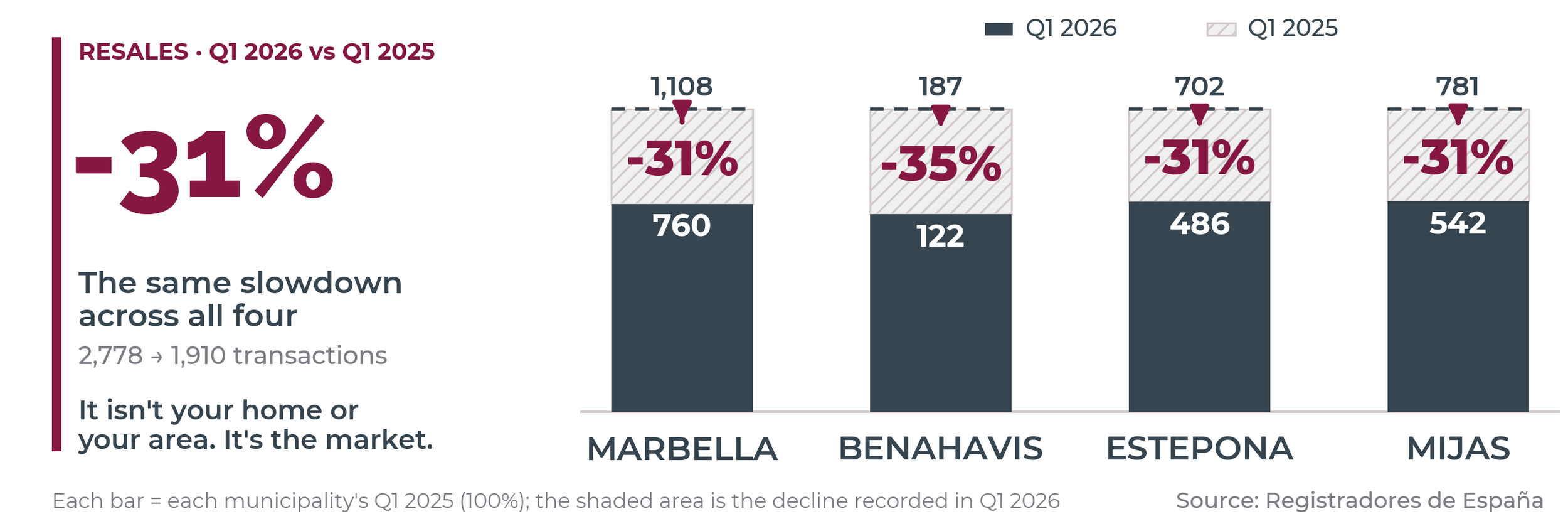

EL MERCADO DE LA COSTA DEL SOL HA CAIDO UN 30%: QUÉ SIGNIFICA PARA EL PRECIO DE TU CASA EN 2026

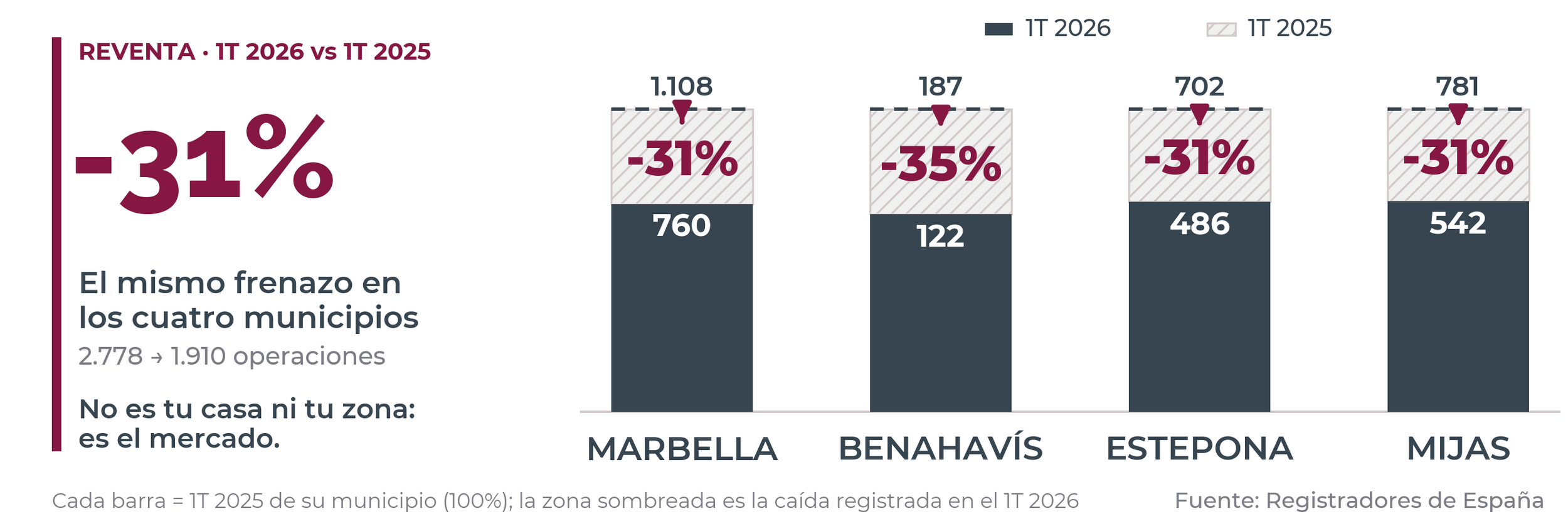

Desde hace unos meses no paran de hacerme la misma pregunta: ¿Qué le pasa al mercado? La respuesta honesta está en el gráfico de abajo. En el primer trimestre de 2026 las ventas de segunda mano cayeron en torno a un tercio respecto al mismo trimestre de 2025 por lo que, siendo el mismo periodo, la caída es real y no el típico arranque lento de principios de año. Entre los cuatro municipios supone unas 870 ventas menos en un solo trimestre, de 2.778 a 1.910. Son ya datos, y no sensaciones que ya teníamos, y que se pueden traducir en lo siguiente:

1. Todo el mercado se ha frenado a la vez. Marbella, Benahavís, Estepona y Mijas caen entre un 31% y un 35%. Cuando cuatro zonas distintas se mueven casi igual, la causa no es local: no es una calle, ni un edificio, ni un tipo de vivienda, es la situación general: los tipos de interés, la financiación más difícil, la situación internacional y el comprador que se toma su tiempo.

2. El mercado esta más lento y ahora manda el comprador. Menos ventas significan que las viviendas tardan más en venderse y el stock se acumula. Lo que antes se vendía en semanas ahora puede tardar meses. Cuando la oferta se mantiene y la demanda baja, el equilibrio cambia. Hemos pasado de un mercado de vendedores a un mercado de compradores. Si estás comprando, es tu momento para tomarte tu tiempo y negociar con calma. Pero no hay que confundir un mercado más lento con un mercado barato. Las buenas viviendas bien valoradas se siguen vendiendo rápido y los compradores serios se las quedan.

3. En este mercado, el precio de salida es la única palanca que cuenta. Cuando el comprador tiene opciones, la vivienda deja de competir y compite el precio. Una vivienda bien valorada desde el primer día se sigue vendiendo bien: en mi experiencia, en menos de 90 días y con menos de un 3% de descuento. Una vivienda con un precio demasiado alto hace lo contrario: persigue al mercado a la baja, pierde sus mejores semanas y se vende más tarde y por menos. Por eso no acepto propiedades sobrevaloradas: no ayudan y cuestan dinero sin darse cuenta.

En resumen, el mercado no se ha hundido aunque las viviendas tardan más en venderse que hace un año. Lo que si estoy vigilando ahora es cuánto tardan en venderse y si el stock sin vender sigue creciendo en verano. En cualquier caso, el vendedor que acepta el nuevo ritmo y pone precio de hoy seguirá vendiendo bien mientras el que se aferra a los precios del año pasado esperará meses y acabará persiguiendo al mercado a la baja.

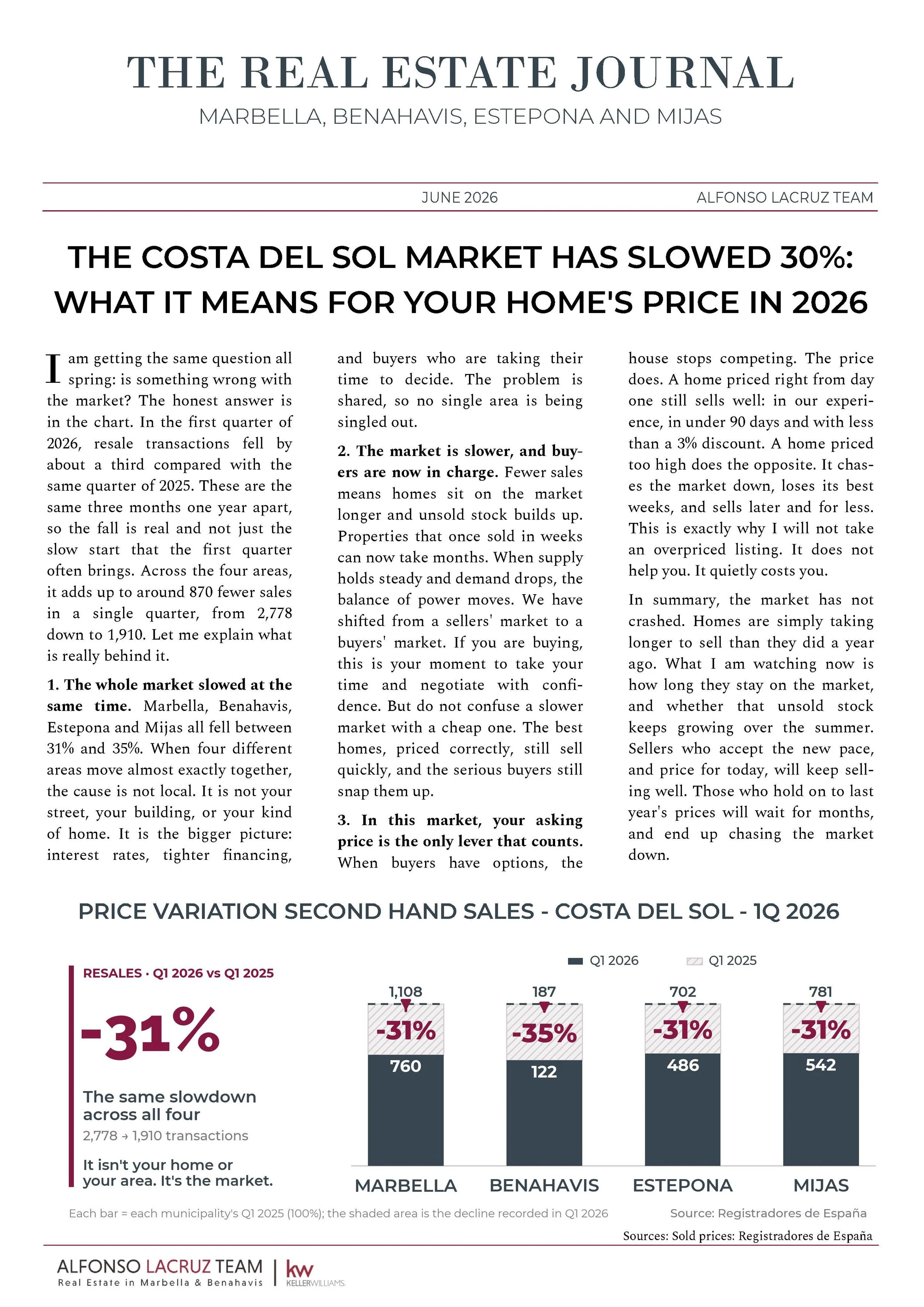

THE COSTA DEL SOL MARKET HAS SLOWED 30%: WHAT IT MEANS FOR YOUR HOME'S PRICE IN 2026

I am getting the same question all spring: is something wrong with the market? The honest answer is in the chart. In the first quarter of 2026, resale transactions fell by about a third compared with the same quarter of 2025. These are the same three months one year apart, so the fall is real and not just the slow start that the first quarter often brings. Across the four areas, it adds up to around 870 fewer sales in a single quarter, from 2,778 down to 1,910. Let me explain what is really behind it.

1. The whole market slowed at the same time. Marbella, Benahavis, Estepona and Mijas all fell between 31% and 35%. When four different areas move almost exactly together, the cause is not local. It is not your street, your building, or your kind of home. It is the bigger picture: interest rates, tighter financing, and buyers who are taking their time to decide. The problem is shared, so no single area is being singled out.

2. The market is slower, and buyers are now in charge. Fewer sales means homes sit on the market longer and unsold stock builds up. Properties that once sold in weeks can now take months. When supply holds steady and demand drops, the balance of power moves. We have shifted from a sellers' market to a buyers' market. If you are buying, this is your moment to take your time and negotiate with confidence. But do not confuse a slower market with a cheap one. The best homes, priced correctly, still sell quickly, and the serious buyers still snap them up.

3. In this market, your asking price is the only lever that counts. When buyers have options, the house stops competing. The price does. A home priced right from day one still sells well: in our experience, in under 90 days and with less than a 3% discount. A home priced too high does the opposite. It chases the market down, loses its best weeks, and sells later and for less. This is exactly why I will not take an overpriced listing. It does not help you. It quietly costs you.

In summary, the market has not crashed. Homes are simply taking longer to sell than they did a year ago. What I am watching now is how long they stay on the market, and whether that unsold stock keeps growing over the summer. Sellers who accept the new pace, and price for today, will keep selling well. Those who hold on to last year's prices will wait for months, and end up chasing the market down.

RENOVATED OR TO RENOVATE IN MARBELLA & BENAHAVIS? WHAT'S WORTH IT IN 2026

It's one of the most common dilemmas I hear from buyers in this price range: pay more for a fully renovated home and move in within weeks, or pay less for one with potential and take on months of building work. There is no single right answer, and having walked both roads with clients, I know each option comes with fine print worth reading before you commit.

1. Peace of mind has a price tag. A move-in-ready home includes something no spreadsheet captures: certainty. You know how it will look, when you'll move in, and exactly what it costs. That certainty has a clear cost: the profit margin of the developer or investor who took on the work before you, along with their time, capital tied up, and the risk that something might have gone wrong. It's a fair premium, the job is done and the result speaks for itself, but it's worth keeping in mind when comparing with an unrenovated alternative.

2. Renovating can pay off… or not. Buying to renovate can be a smart move, but only if the location, the property, and the community all line up. In numbers, a quality full renovation in Marbella or Benahavís typically runs between €1,500 and €2,500 per square metre, and overruns of 15-25% are common when no experienced hand is steering the project. Old pipes show up the moment walls come down, permits drag on, design choices shift mid-build. Add the time cost: months without enjoying the house, often paying rent elsewhere in the meantime. When everything aligns, the savings are real and the home turns out exactly as you wanted; when it doesn't, the opportunity ends up costing as much as the turnkey option, or more.

3. Before you decide, look at what isn't on display. Inspect the roof, plumbing, and walls before falling for the kitchen. Ask for a fixed written quote, not a verbal estimate. And check what the community allows: many gated developments here have their own renovation rules, and not all of them permit the same scope of work. If permits are involved, find out the real timelines at the town hall as they rarely match the calendar you have in mind. Those who know what they want and how hard they're willing to work for it succeed with either path. Those who don't, fail at both.

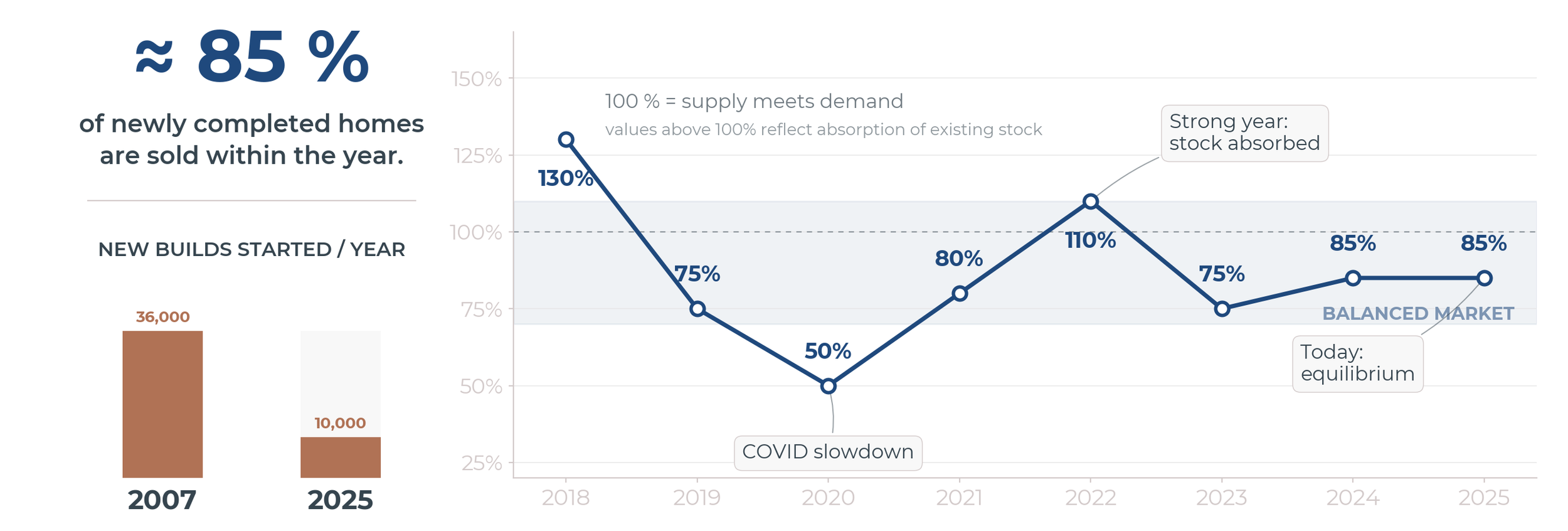

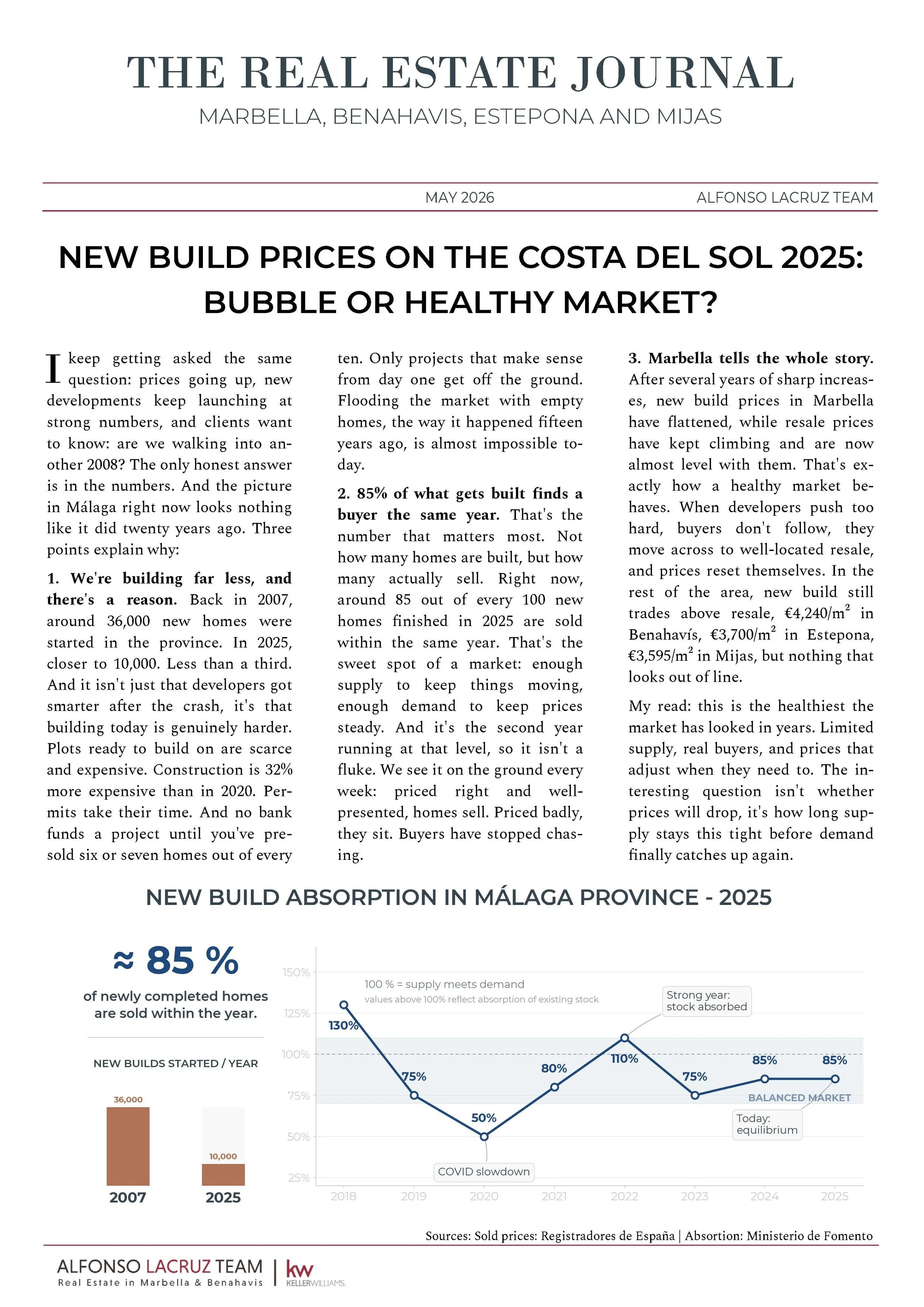

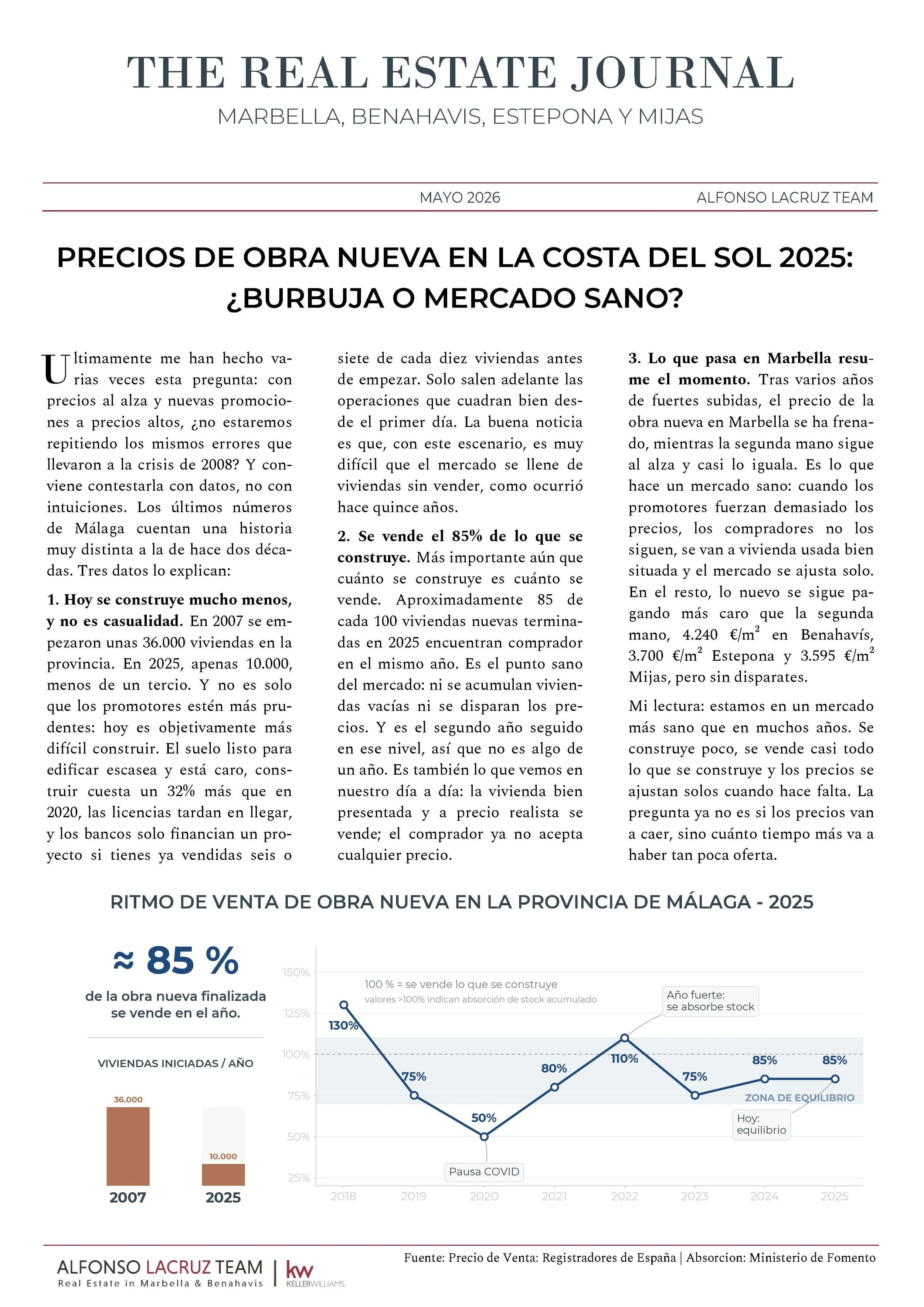

NEW BUILD PRICES ON THE COSTA DEL SOL 2025: BUBBLE OR HEALTHY MARKET?

I keep getting asked the same question: prices going up, new developments keep launching at strong numbers, and clients want to know: are we walking into another 2008? The only honest answer is in the numbers. And the picture in Málaga right now looks nothing like it did twenty years ago. Three points explain why:

1. We're building far less, and there's a reason. Back in 2007, around 36,000 new homes were started in the province. In 2025, closer to 10,000. Less than a third. And it isn't just that developers got smarter after the crash, it's that building today is genuinely harder. Plots ready to build on are scarce and expensive. Construction is 32% more expensive than in 2020. Permits take their time. And no bank funds a project until you've presold six or seven homes out of every ten. Only projects that make sense from day one get off the ground. Flooding the market with empty homes, the way it happened fifteen years ago, is almost impossible today.

2. 85% of what gets built finds a buyer the same year. That's the number that matters most. Not how many homes are built, but how many actually sell. Right now, around 85 out of every 100 new homes finished in 2025 are sold within the same year. That's the sweet spot of a market: enough supply to keep things moving, enough demand to keep prices steady. And it's the second year running at that level, so it isn't a

fluke. We see it on the ground every week: priced right and wellpresented, homes sell. Priced badly, they sit. Buyers have stopped chasing.

3. Marbella tells the whole story. After several years of sharp increases, new build prices in Marbella have flattened, while resale prices have kept climbing and are now almost level with them. That's exactly how a healthy market behaves. When developers push too hard, buyers don't follow, they move across to well-located resale, and prices reset themselves. In the rest of the area, new build still trades above resale, €4,240/m² in Benahavís, €3,700/m² in Estepona, €3,595/m² in Mijas, but nothing that looks out of line.

My read: this is the healthiest the market has looked in years. Limited supply, real buyers, and prices that

adjust when they need to. The interesting question isn't whether prices will drop, it's how long supply stays this tight before demand finally catches up again.

¿COMPRAR CASA REFORMADA O PARA REFORMAR EN MARBELLA Y BENAHAVÍS? ¿QUÉ CONVIENE MÁS?

Es una de las dudas que más veces escucho en esta franja de precio: pagar más por una casa ya reformada y entrar a vivir en pocas semanas, o pagar menos por una con potencial y asumir los meses de obra. No hay una respuesta buena para todos, y habiendo acompañado a clientes por ambos caminos, sé que cada opción tiene su letra pequeña y conviene leerla antes de decidir.

1. La tranquilidad cuesta dinero. Una casa lista para entrar incluye algo que no aparece en ningún número: la certeza. Sabes cómo va a quedar, cuándo te mudas y cuánto te cuesta. Esa tranquilidad tiene un coste claro: el beneficio del promotor o inversor que asumió la obra está incluido en el precio, junto con el tiempo invertido, el capital inmovilizado y el riesgo de que algo saliera mal. Es una prima razonable, el trabajo está hecho y el resultado se ve, pero conviene tenerla presente al comparar con una opción sin reformar.

2. Reformar puede salir bien… o no. Comprar para reformar puede ser una buena operación, pero solo si la zona, la casa y la comunidad acompañan. En cifras, una reforma integral con buen nivel en Marbella y Benahavís suele costar entre 1.500 € y 2.500 € el metro cuadrado, y los sobrecostes rondan el 15-25 % si nadie con experiencia controla la obra. Aparecen tuberías viejas al picar, permisos que tardan, decisiones que cambian sobre la marcha. A esto hay que sumarle el tiempo: meses sin disfrutar la casa y, a menudo, viviendo en otra mientras tanto. Cuando todo encaja, el ahorro es real y la casa queda exactamente como uno la quería; cuando no, la oportunidad acaba costando lo mismo que la casa ya reformada, o más.

3. Antes de decidir, mira lo que no se ve. Revisa tejado, tuberías y muros antes que la cocina. Pide presupuesto cerrado por escrito, no a ojo. Y pregunta qué deja hacer la comunidad: aquí muchas urbanizaciones cerradas tienen su propio reglamento de obras y no todas permiten lo mismo. Si pides licencias, infórmate de los plazos reales del ayuntamiento, que rara vez coinciden con los del calendario. Quien sabe lo que quiere y cuánto está dispuesto a pelearlo, acierta con cualquiera de las dos opciones. Quien no, se equivoca con las dos.

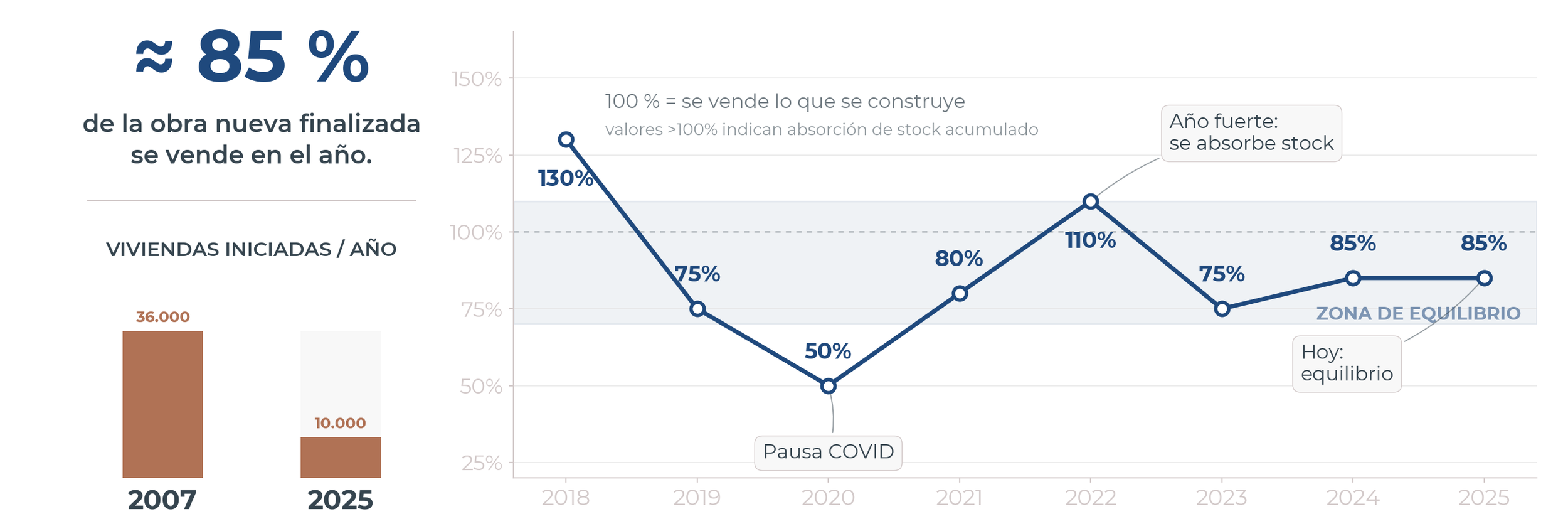

PRECIOS DE OBRA NUEVA EN LA COSTA DEL SOL 2025: ¿BURBUJA O MERCADO SANO?

Ultimamente me han hecho varias veces esta pregunta: con precios al alza y nuevas promociones a precios altos, ¿no estaremos repitiendo los mismos errores que llevaron a la crisis de 2008? Y conviene

contestarla con datos, no con intuiciones. Los últimos números de Málaga cuentan una historia muy distinta a la de hace dos décadas. Tres datos lo explican:

1. Hoy se construye mucho menos, y no es casualidad. En 2007 se empezaron unas 36.000 viviendas en la

provincia. En 2025, apenas 10.000, menos de un tercio. Y no es solo que los promotores estén más prudentes: hoy es objetivamente más difícil construir. El suelo listo para edificar escasea y está caro, construir cuesta un 32% más que en 2020, las licencias tardan en llegar, y los bancos solo financian un proyecto si tienes ya vendidas seis osiete de cada diez viviendas antes de empezar. Solo salen adelante las operaciones que cuadran bien desde el primer día. La buena noticia es que, con este escenario, es muy difícil que el mercado se llene de viviendas sin vender, como ocurrió hace quince años.

2. Se vende el 85% de lo que se construye. Más importante aún que cuánto se construye es cuánto se

vende. Aproximadamente 85 de cada 100 viviendas nuevas terminadas en 2025 encuentran comprador

en el mismo año. Es el punto sano del mercado: ni se acumulan viviendas vacías ni se disparan los precios.

Y es el segundo año seguido en ese nivel, así que no es algo de un año. Es también lo que vemos en

nuestro día a día: la vivienda bien presentada y a precio realista se vende; el comprador ya no acepta cualquier precio.

3. Lo que pasa en Marbella resume el momento. Tras varios años de fuertes subidas, el precio de la obra nueva en Marbella se ha frenado, mientras la segunda mano sigue al alza y casi lo iguala. Es lo que hace un mercado sano: cuando los promotores fuerzan demasiado los precios, los compradores no los siguen, se van a vivienda usada bien situada y el mercado se ajusta solo. En el resto, lo nuevo se sigue pagando más caro que la segunda mano, 4.240 €/m² en Benahavís, 3.700 €/m² Estepona y 3.595 €/m² Mijas, pero sin disparates.

Mi lectura: estamos en un mercado más sano que en muchos años. Se construye poco, se vende casi todo lo que se construye y los precios se ajustan solos cuando hace falta. La pregunta ya no es si los precios van a caer, sino cuánto tiempo más va a haber tan poca oferta.

Journal on the Real Estate Market on the Costa del Sol - May 2026

Journal sobre el mercado inmobiliario de la Costa de Sol - Mayo 2026

SALES FELL, PRICES ROSE: MARBELLA & COSTA DEL SOL Q4 2025. SHOULD YOU BUY, SELL OR INVEST IN 2026?

What the latest data means for sellers, buyers and investors?

Sales fell. Prices rose. In Q4 2025, the Costa del Sol delivered a contradiction that tells a different story to each of the three readers who matter most: the seller thinking of listing, the buyer still hesitating, and the investor de-ciding where to allocate next.

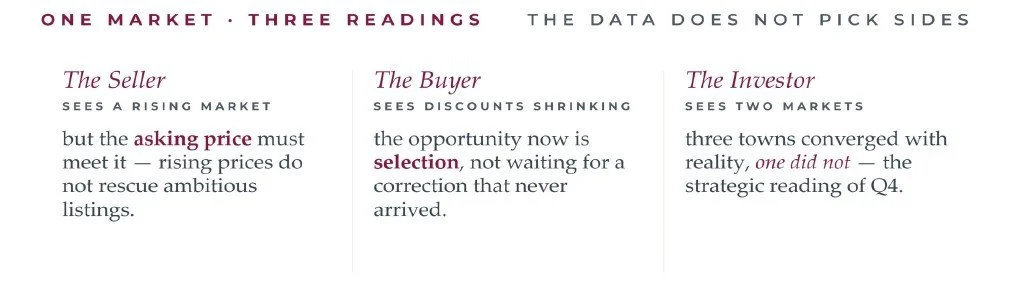

For the Seller. The official figures are encouraging: sold prices climbed across all four municipalities, and the gap between asking and sold prices is narrowing in Marbella, Benahavís and Estepona. That only happens when realistic sellers meet the market and ambitious ones do not. A property that has been listed for many months without movement is not being failed by the market, it is being failed by its asking price.

For the Buyer. The room for meaningful negotiation is shrinking. In Marbella, sold prices rose 3.2% in Q4 alone while asking prices rose only 2.1% so the real market is moving faster than seller expectations. On properties priced sensibly from day one, the ones that actually transact, discounts have become minimal. The correc-tion some buyers were waiting for has not arrived, and the window for waiting productively is narrowing with each quarter. The opportunity now lies in selection: identifying the right property in the right micro-location at a fair price, rather than holding out for a discount the data no longer supports.

For the Investor. The most useful signal this quarter is the divergence between Mijas and the other three mu-nicipalities. In Marbella, Benahavís and Estepona, the gaps between asking and sold prices stand at 31.4%, 42.5% and 23.9% respectively, all trending downward. These are markets where reality has been absorbed, and disciplined entry is rewarded over speculative timing.

Mijas is the exception: the gap is only 8.5%, but it is widening rather than closing, with asking prices rising fast-er than sold prices. That is not an opportunity, it is a market where sellers have not yet adjusted. The disciplined approach is to watch it closely and enter only with precision, zone by zone, rather than on aggregate numbers.

One market. Three readings. The data does not pick sides, the reader does.

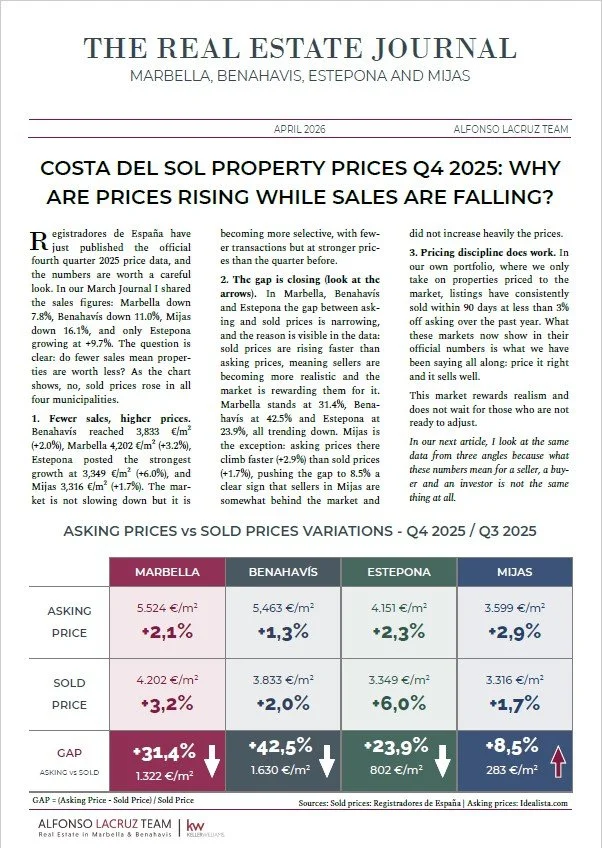

COSTA DEL SOL PROPERTY PRICES Q4 2025: WHY ARE PRICES RISING WHILE SALES ARE FALLING?

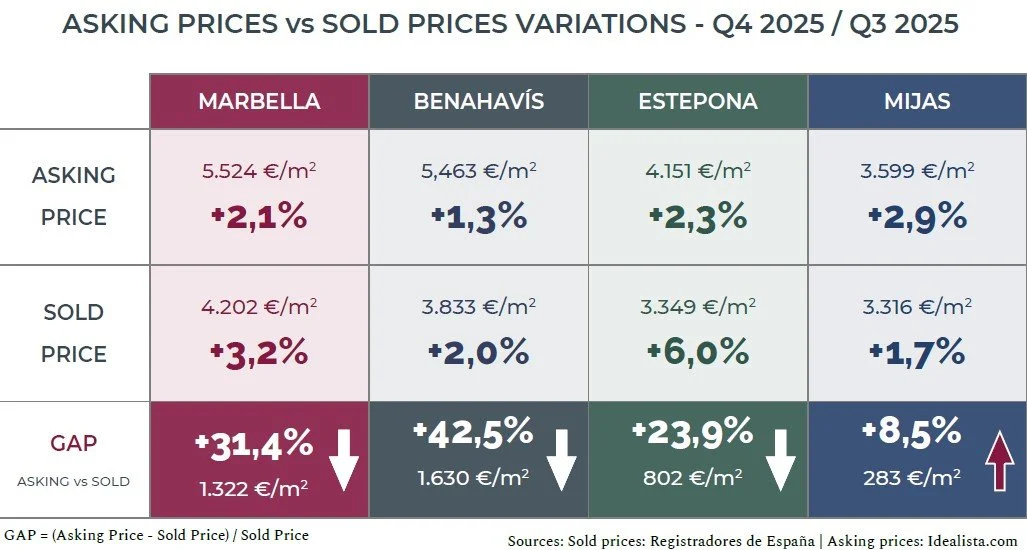

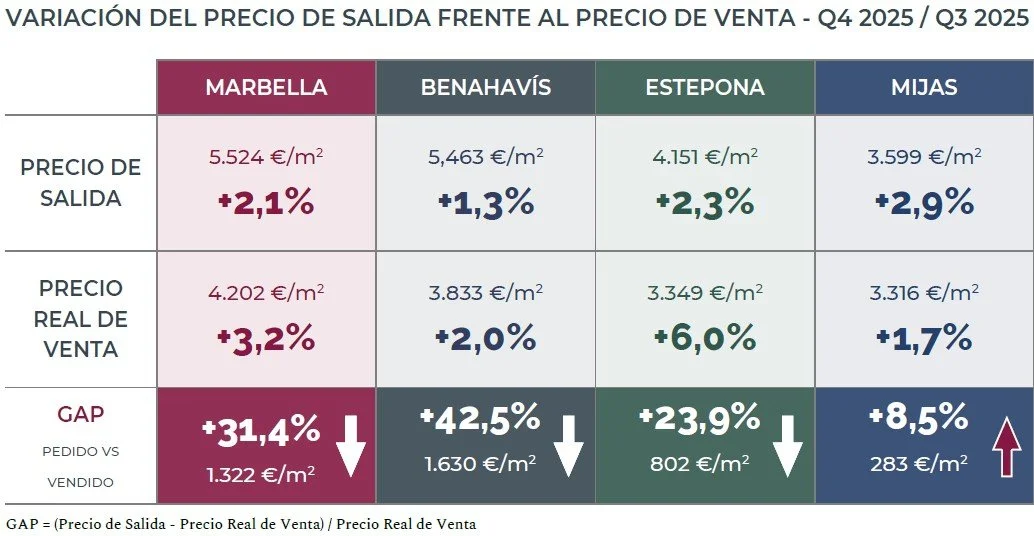

Registradores de España have just published the official fourth quarter 2025 price data, and the numbers are worth a careful look. In our March Journal I shared the sales figures: Marbella down 7.8%, Benahavís down 11.0%, Mijas down 16.1%, and only Estepona growing at +9.7%. The question is clear: do fewer sales mean proper-ties are worth less? As the chart shows, no, sold prices rose in all four municipalities.

1. Fewer sales, higher prices. Benahavís reached 3,833 €/m² (+2.0%), Marbella 4,202 €/m² (+3.2%), Estepona posted the strongest growth at 3,349 €/m² (+6.0%), and Mijas 3,316 €/m² (+1.7%). The market is not slowing down but it is becoming more selective, with fewer transactions but at stronger prices than the quarter before.

2. The gap is closing (look at the arrows). In Marbella, Benahavís and Estepona the gap between ask-ing and sold prices is narrowing, and the reason is visible in the data: sold prices are rising faster than asking prices, meaning sellers are becoming more realistic and the market is rewarding them for it. Marbella stands at 31.4%, Benahavís at 42.5% and Estepona at 23.9%, all trending down. Mijas is the exception: asking prices there climb faster (+2.9%) than sold prices (+1.7%), pushing the gap to 8.5% a clear sign that sellers in Mijas are somewhat behind the market and did not increase heavily the prices.

3. Pricing discipline does work. In our own portfolio, where we only take on properties priced to the market, listings have consistently sold within 90 days at less than 3% off asking over the past year. What these markets now show in their official numbers is what we have been saying all along: price it right and it sells well.

This market rewards realism and does not wait for those who are not ready to adjust.

In our next article, I look at the same data from three angles because what these numbers mean for a seller, a buyer and an investor is not the same thing at all.

Mercado Inmobiliario Marbella y la Costa del Sol T4 2025 ¿Vender, Comprar o Invetir?

Bajaron las ventas. Subieron los precios. En el cuarto trimestre de 2025, la Costa del Sol dejó una contradicción que cuenta una historia distinta dependiendo de desde donde se mire: el propietario que valora vender, el comprador que estudia comprar, y el inversor que decide dónde colocar su capital.

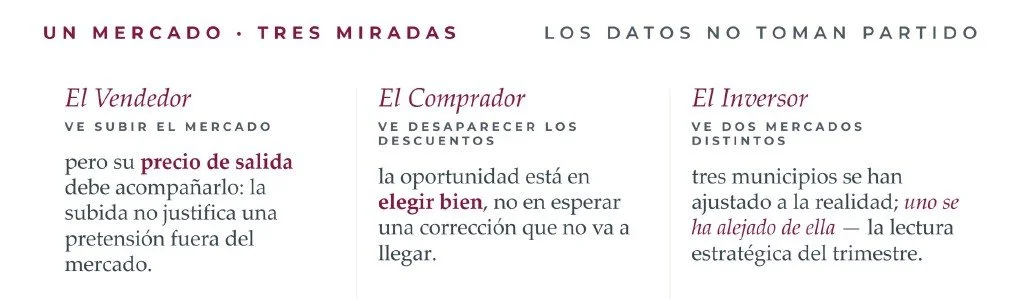

Para el Vendedor. Las cifras oficiales son buenas: los precios de venta subieron en los cuatro municipios, y la brecha entre precio de salida y precio real se estrecha en Marbella, Benahavís y Estepona. Eso solo ocurre cuando los vendedores que son realistas se ajustan al mercado mientras que los ambiciosos no lo hacen. Cuando una propiedad lleva meses sin moverse, el problema no es el mercado: es el precio.

Para el Comprador. El margen real de negociación se está cerrando. En Marbella, los precios de venta subieron un 3,2% en el cuarto trimestre mientras los de salida solo un 2,1% lo que significa que el mercado real crece más rápido que las expectativas del vendedor. En las propiedades que entran al mercado bien valoradas desde el primer día, los descuentos son ya mínimos. La corrección que algunos compradores podían estar esperando no ha llegado, y la oportunidad de seguir esperando se está cerrando según pasa el tiempo. La clave hoy está en la selección, es decir, identificar la propiedad adecuada en la microzona correcta y no en esperar un descuento que los datos ya no parecen respaldar.

Para el Inversor. La señal más interesante este trimestre es la divergencia entre Mijas y el resto. En Marbella, Benahavís y Estepona, las brechas entre precio de salida y venta son del 31,4%, 42,5% y 23,9% respectivamente y con todas ellas tendiendo a bajar. Mercados donde los vendedores ya han ajustado expectativas, y donde hoy se pre-mia la disciplina, no la especulación. Mijas es la excep-ción: la brecha es solo del 8,5%, pero se amplía en lugar de cerrarse. Eso no es una oportunidad sino un mercado donde los vendedores aún no han tenido que ajustarse porque el margen todavía es razonable. La clave, de nue-vo, es observar y entrar con precisión, estudiando pre-cios y oportunidades urbanización por urbanización y no basar los precios en las medias de los municipios.

Un mercado. Tres lecturas. Los datos no toman partido, el lector sí.

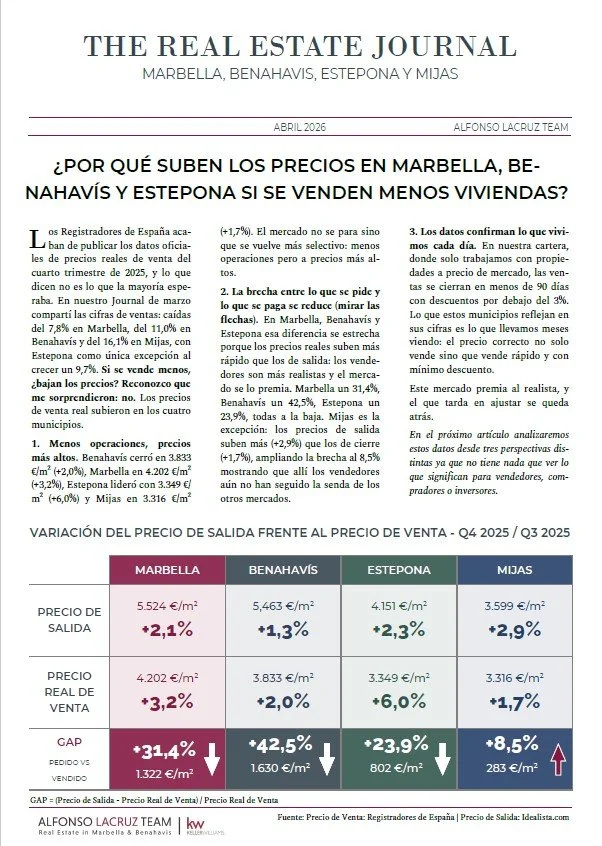

¿Por qué suben los precios en Marbella, Benahavís y Estepona si se venden menos viviendas?

Los Registradores de España acaban de publicar los datos oficiales les de precios reales de venta del cuarto trimestre de 2025, y lo que dicen no es lo que la mayoría esperaba.

En nuestro Journal de marzo compartí las cifras de ventas: caídas del 7,8% en Marbella, del 11,0% en Benahavís y del 16,1% en Mijas, con Estepona como única excepción al crecer un 9,7%.

Si se vende menos, ¿bajan los precios? Reconozco que me sorprendieron: no. Los precios de venta real subieron en los cuatro municipios.

1. Menos operaciones, precios más altos. Benahavís cerró en 3.833€/m² (+2,0%), Marbella en 4.202 €/m² (+3,2%), Estepona lideró con 3.349 €/m² (+6,0%) y Mijas en 3.316 €/m² (+1,7%). El mercado no se para sino que se vuelve más selectivo: menos operaciones pero a precios más altos.

2. La brecha entre lo que se pide y lo que se paga se reduce (mirar las flechas). En Marbella, Benahavís y Estepona esa diferencia se estrecha porque los precios reales suben más rápido que los de salida: los vende-dores son más realistas y el merca-do se lo premia. Marbella un 31,4%, Benahavís un 42,5%, Estepona un 23,9%, todas a la baja. Mijas es la excepción: los precios de salida suben más (+2,9%) que los de cierre (+1,7%), ampliando la brecha al 8,5%mostrando que allí los vendedores aún no han seguido la senda de los otros mercados.

3. Los datos confirman lo que vivimos cada día. En nuestra cartera, donde solo trabajamos con propie-dades a precio de mercado, las ven-tas se cierran en menos de 90 días con descuentos por debajo del 3%. Lo que estos municipios reflejan en sus cifras es lo que llevamos meses viendo: el precio correcto no solo vende sino que vende rápido y con mínimo descuento.

Este mercado premia al realista, y el que tarda en ajustar se queda atrás.

En el próximo artículo analizaremos estos datos desde tres perspectivas dis-tintas ya que no tiene nada que ver lo que significan para vendedores, com-pradores o inversores.

Journal sobre el mercado inmobiliario de la Costa del Sol - Abril 2026

Journal on the Real Estate Market on the Costa del Sol - April 2026

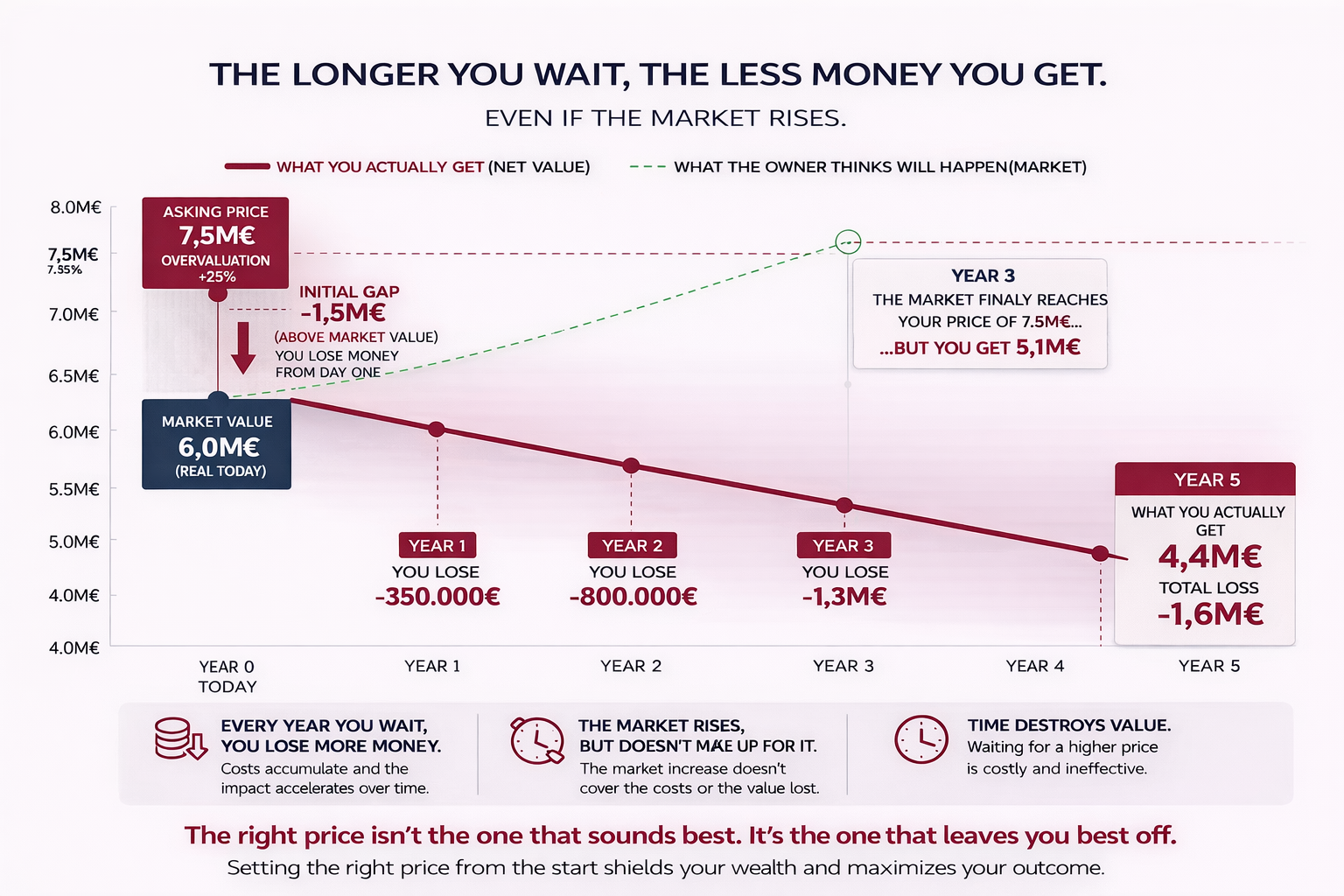

WHAT HAPPENS WHEN YOU OVERPRICE A PROPERTY: HOW TO LOSE VALUE EVEN IN A RISING MARKET ?

Overpricing a property can reduce what you actually walk away with, even in a rising market. If the property does not generate rental income, waiting is not neutral. In most cases, it quietly works against you. This is especially relevant in markets like Marbella and Benahavís, where many owners assume future price growth will compensate for an ambitious asking price. The reality is different.

Why overpricing a property can cost sellers money?

When a property is launched above its true market val-ue, five factors start working in parallel:

1. Market growth. Yes, prices may increase over time. This is often the reason behind overpricing. But it is on-ly one variable and not the most decisive one.

2.Holding costs. Owning a property comes with ongoing expenses, whether it is sold or not. Community fees, insurance, maintenance and upkeep continue every month. A realistic assumption is around 1.5% per year.

3. Inflation. Even if you achieve a higher price in the future, the real value of that money may be lower. Infla-tion reduces purchasing power over time, often as-sumed at around 2% annually.

4. Opportunity cost. The capital tied up in the property could be working elsewhere. Even a conservative return of 4% per year compounds over time, increasing the cost of waiting.

5. Property ageing. Properties lose relative appeal over time. Design trends evolve, competition improves, and even well-maintained homes can feel outdated. A rea-sonable estimate is around 1% per year.

While the market may rise, these factors ac-cumulate. The result is simple: overpricing does not protect value, it often reduces it. The right asking price is not the highest number a property could reach. It is the price that protects what you actually receive.

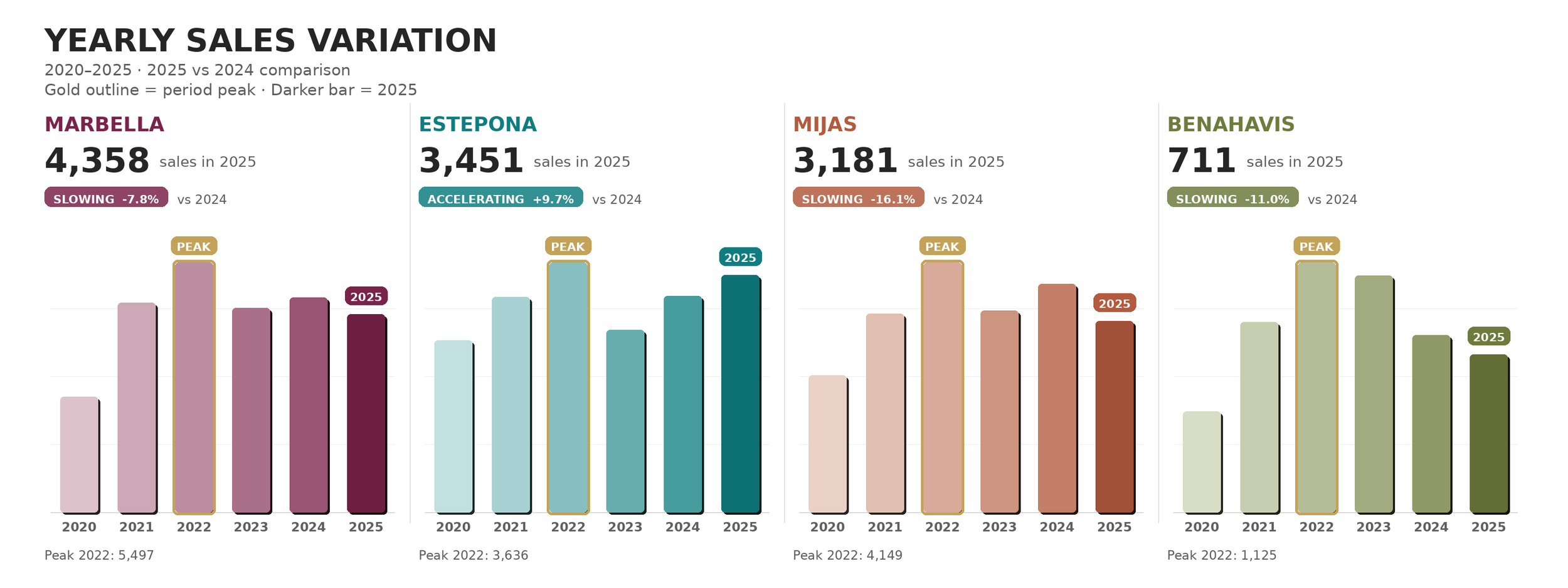

MARKET STABILITY? ESTEPONA RISES WHILE MARBELLA, BENAHAVÍS, AND MIJAS SALES FALL

The latest sales figures from the fourth quarter of 2025 recently published confirm the Costa del Sol property market is changing pace. The exceptional momentum of recent years is easing, but this should not be mistaken for weak-ness. Instead, we are seeing a gradual return to a more balanced market where buyers remain ac-tive but are highly selective.

1. Marbella and Benahavís are slowing, while Estepona advances. The four municipalities are no longer moving together. Marbella recorded a 7.8% drop in homes sold compared with 2024, while Benahavís fell by 11.0% and Mijas by 16.1%. Estepona, however, moved the other way, rising 9.7%. This proves there is no single Costa del Sol market anymore; micro-local dynamics dictate performance.

2. Affordability is only half the story as product mix is key. If price point alone dictated the market, the numbers would look diferent. Mijas, the most accessible area at an average €360,043, saw the sharpest drop. Estepona, averaging €414,976, surged. Why?Estepona is heavily buoyed by a wave of new-build completions from past contracts ï¬nally hitting the Notary. Mijas, conversely, is behaving like a traditional resale market feeling a natural cooling. In higher-end markets like Marbella €734,425) and Benahavís (€939,770), buyers are simply taking more time, carefully comparing luxury resales against a few shiny new-build alternatives.

3. The market still looks strong in historical terms. Despite the recent slowdown, all four municipalities remain well above their 20-year average for sales. The boom years created an unusually high benchmark. Today’s activity repre-sents a healthier, more sustainable rhythm rather than a worrying contraction.

In this complex environment, strategy matters. For homeowners in Marbella and Benahavís, success depends more than ever on expert pricing, strong positioning, and deep market insight. It is the pre-cise difference between merely sitting on the market and success-fully getting sold.